Managed funds are an alternative to purchasing direct investments.

In a managed fund, your money is pooled together with other investors to obtain broader market exposure. It is invested by a professional fund manager in a range of asset classes (e.g. cash, fixed interest, shares) in line with an investment objective. Each investor is allocated a number of ‘units’, each unit representing an equal amount of the market value of a fund. If the value of the fund increases, the unit price will rise and vice versa.

During the year you are usually paid income or ‘distributions’ periodically while the value of your investment will rise and fall with the value of your underlying assets.

There are thousands of managed funds on the market today. You can invest in asset-specific funds such as share funds, property funds and bond funds. You can invest in a fund that focuses on local, or global assets. Or you can select a ‘balanced’ fund or ‘growth’ fund that combines some or all of the different asset classes.

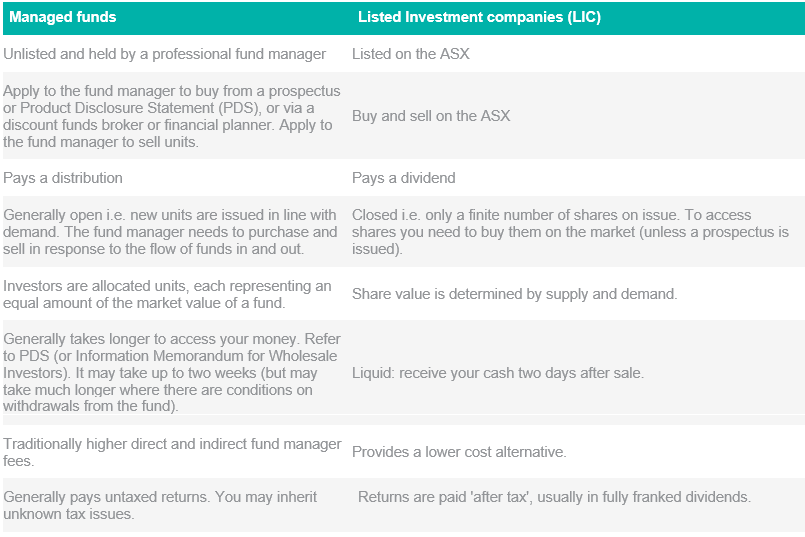

Listed versus unlisted managed funds

Managed funds are unlisted, whereas listed investment companies (LICs) are listed and traded on the sharemarket via your broker. To help you determine what suits you, we’ve summarised below some of the differences you will find between unlisted and listed funds:

Why consider managed funds

- Easily diversify your investment portfolio across different asset classes, companies, industries, sectors and countries.

- Investment decisions are managed by an experienced professional investor who has access to information, research and investment processes not easily available to individual investors.

- As you are sharing the investment with others, you don’t need a large investment sum upfront, you can access certain investments at a fraction of the cost of direct , and you can access large minimum investments.

- Access markets not accessible via the ASX.

- Invest for income (paid to you as a distribution), growth (when the unit price increases in value) or both.

- Where appropriate, may be used in strategies as a ‘set and forget’ investment requiring minimal involvement.

- Many unlisted funds offer savings plans, i.e. after investing an initial lump sum – as low as $1000 in some cases – you can contribute a set, smaller amount, e.g. $100 each month.

Look out for

- Fund managers charge you direct and indirect fees. These fees vary from fund to fund and can substantially affect your long-term returns.

- Once you’ve selected the style of investment, you don’t have control or a say over your investment choices.

- There may be unknown tax issues. You may inherit tax liabilities on gains you didn’t benefit from, and in a period of poor performance, new investors can dilute any unrealised tax losses.

- Capital losses in a managed fund cannot be distributed to you to offset any capital gains outside the fund.

- For ‘open’ managed funds, purchases and sales will have to be made due to the flow of funds in and out (when investors invest or cash in their units), sometimes at less than optimal times.

- High performing managed funds may attract a flock of investors which means the fund could be buying assets when they are expensive. If a downturn happens and investors withdraw, the forced selling may push asset prices down further creating a flurry of redemptions.

- The fund might impose conditions on your withdrawal rights, e.g. freeze withdrawals if they don’t have enough cash to pay them, or in times of high redemptions, there might be a limit on the number of units you can cash out.